Bobby Jindal’s new tax plan isn’t getting all the buzz that Trump’s got, perhaps because he’s much lower in the polls. But I thought you should see it.

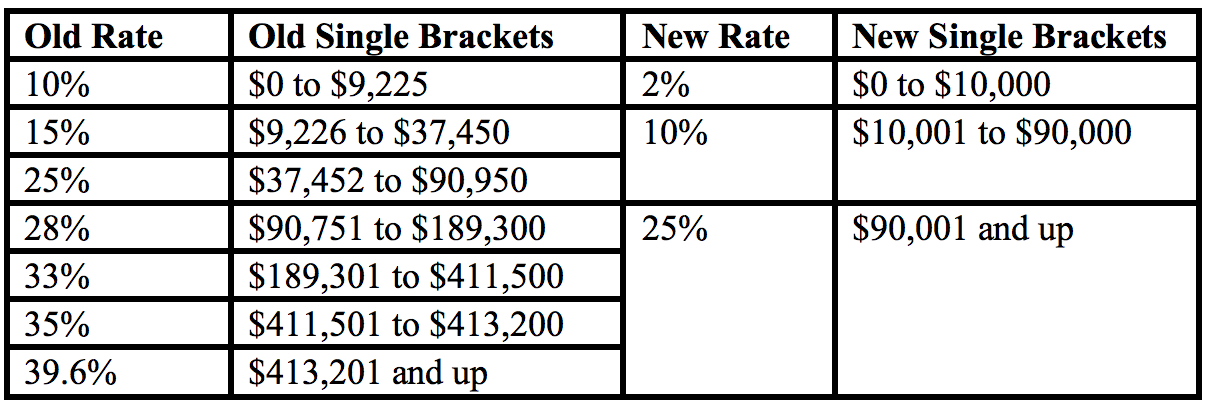

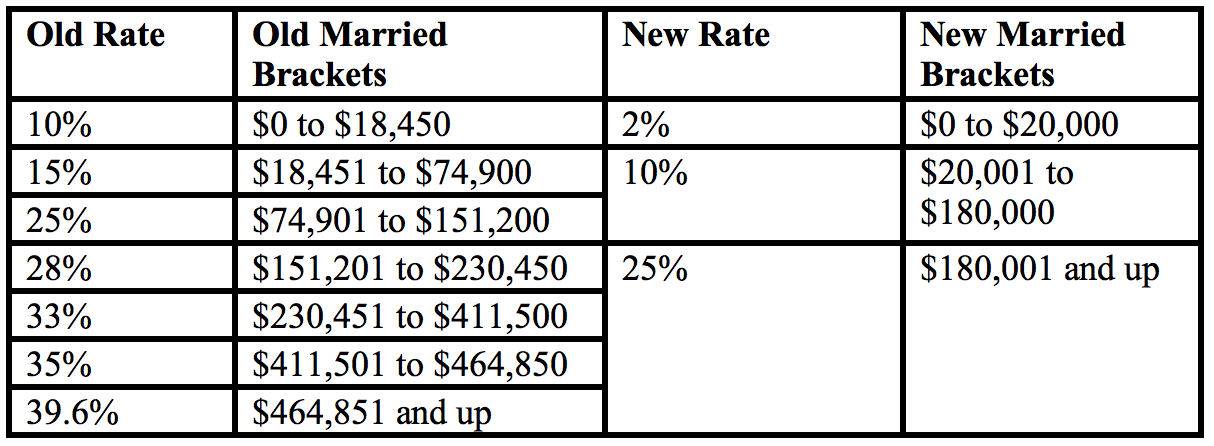

The big takeaways from it are that Jindal switches to a three rate tax system, 2 percent, 10 percent, and 25 percent. Everybody pays taxes in his system. Everybody.

He also eliminates the corporate tax completely and taxes capital gains and dividends as ordinary income.

Here are his new ‘ordinary income’ tax brackets for singles and married couples:

Everybody gets a big tax cut except those who don’t pay taxes now. I’m sure this won’t go over well with the left.

Here’s the lowdown on personal taxes via his plan:

Personal Income Tax Changes In Governor Jindal’s Tax Reform Plan:

Reduce brackets from 7 to 3 and simplify filing status to two: single and married. Maintain widower filing jointly.

- Eliminate the personal exemption, the standard deduction and all itemized deductions, except for five:

– The charitable contributions deduction with no changes.

– The Earned Income Tax Credit, transferred over to the payroll tax where it will be easier to audit, administered by employers, and more appropriately mirror income

– The Mortgage Interest Deduction, capped at interest on mortgages worth up to $500,000 instead of $1 million as is allowed today

– Replace the exclusion for employer-based health insurance with a standard deduction for health insurance costs whether they are provided by the employer or purchased by an individual

– A nonrefundable dependents credit that accounts for household size of dependents: children under the age of 18, elderly making less than $5,000 over the age of 65, and the disabled.

- These remaining deductions would have no PEP or Pease limitation, while imposes arbitrary income caps on the value of deductions.

- Eliminate the Alternative Minimum Tax, which increasingly penalizes the middle class.

- Address the marriage penalty by doubling income brackets for married vs. individual filers and allowing married filers to chose how to file. Currently, the married brackets are not double the single brackets, which means that a second working spouse can increase the couple’s tax rate and lower overall after-tax income.

– For example, John Doe currently makes $65,000. He falls into the 25% bracket as a single man and the 15% bracket as a married man. If his wife, Jane Doe, starts to work and makes only $8,000 a year at a part time job, they would still fall into the 15% bracket as a married couple and pay $1,200 more in taxes. If Jane gets a fulltime job making $50,000 per year, now Joe and Jane fall into the 25% bracket, and they have to pay for childcare. So they pay 12,500 more in taxes plus an additional $5,000 per year in childcare.

There’s much more you can read about his tax plan at his website.